SPEAKER_03: Did you just finish a good cry because you have this wetness right here on your eye? Oh, sorry. I just got out of my cold

SPEAKER_01: plunge in my sauna because you know, I hit a new record low weight 169 this week. Oh, hold on. What's your temperature on?

SPEAKER_01: I don't want to say it's embarrassing. It's embarrassing. I don't want to say no, what is it? I've been doing like 56 58. But it's great. It's okay. I mean, all these lunatics like I don't know, they're at 45 degrees 48 degrees. I think it's unnecessary. You get the same value. I think my two year old does it. It's good. It's really

SPEAKER_03: impressive.

SPEAKER_05: I consider an 80 degree pool to be a cold plunge. I don't get it unless it's like 85.

SPEAKER_02: I've been to pool parties at Sax's house. There's no difference between it's a full on schmitz.

SPEAKER_03: It's a schmitz. If it's not the temperature of bathwater, I

SPEAKER_05: don't get it.

SPEAKER_03: Yeah.

SPEAKER_01: Yeah, it's just got schmitz. It's crazy. And then I went in my infrared sinus and Abigail in you do the cold then the warm I think you're supposed to do warm than

SPEAKER_03: cold. No, they say end on cold. And so I've been ending on

SPEAKER_01: Yeah, I just do like a site to do cold, warm, cold, cold, warm

SPEAKER_01: cold. Yes. What do you do? Like two minutes? 10 minutes? Two

SPEAKER_03: minutes? Or what do you do? Yeah, exactly. Like one or two minutes cold plunge. Four

SPEAKER_01: minutes, you warm up, you get back to it. And then you jump back in. Yeah, it works pretty good. You know, I have to say my energy level goes way up. Have you been tracking your blood pressure?

SPEAKER_01: I have not. But I have this executive health coach that I'm using. And so that's where I got those ridiculous glasses, the blue lights and my sleep's better. I got some, I've taken some supplements. I'm eating estrogen.

SPEAKER_03: Are you taking more estrogen?

SPEAKER_02: No, estrogen levels are at an all time high for making out with you guys. It just oozes odd to me. No, it turns out, you

SPEAKER_01: know, even at 52, my testosterone is very high. So that's what is your free testosterone? I don't have the number here. But they said it's the the high end of normal. So I was like, should I be shooting up testosterone? They're like, No, you're good. You're good. Just we'll send it over to free Burke. I said, All right, great. Free break.

SPEAKER_03: A lot of people take testosterone in their 50s and 60s. And I've had a couple of my friends in their early 60s start each is it HGH? Human growth? Yeah. Is that right? Not a good idea.

SPEAKER_01: Seems like a really bad idea that off menu stuff. I don't think it's a good idea. I think you gotta be careful with the off menu items. No, I think you can get a prescription for it. Is that right? Yeah. I know. There's a lot of off menu items available to affluent people with the right doctors. And I don't think it's a good idea. I mean, you guys see Bezos, he's jacked. I didn't bring up anybody specifically. He looks great. I think that's just all weights.

SPEAKER_04: Is he gonna be president? I mean, if you had your choice right now between Bezos and Bob

SPEAKER_01: Iger, who would you trust and Biden? I think we know who you

SPEAKER_02: think. I mean, listen, I was talking to some affluent people

SPEAKER_01: and everybody's going to some affluent people. I don't want to say who but the vague is now people are starting to talk the day I think he's hitting the right chords

SPEAKER_04: man. The vague is about to pass to Santa's he will be I think if

SPEAKER_03: you look at the polling right now, New Hampshire, he'll be the clear number two in about four between four and eight weeks from now. That's crazy. That's crazy. And so I think if he becomes a clear number to the, the think of this, it's like, then all of a sudden, all these maga supporters are given Trump, and then Trump with some small feature improvements that are actually pretty meaningful, right? And then they're like, Well, do I want the 80 year old Trump? Or do I want the 38 year old? Right? With like the super features, you know,

SPEAKER_04: I can forgive all of his other issues when he tells me that he's gonna cut the government, the federal government by 75% 75% My gosh sold. So you're on so you're on TV. I want to continue to gather a little data. There's no rush to make a declaration right now. Give me a little bit of time. Chum up. Are you with the vague? Yes, I and the reason is I would love for

SPEAKER_03: it to be RFK and Biden in a debate and then Trump and vvac in a debate so that I could really figure out between RFK and vvac who I would like to vote for. But I think it's been pretty clear that the democrats have chosen to railroad RFK candidacy. It's unfortunate because I don't think we're given a real fair shake and really being able to evaluate him. Yeah, even the detractors like freeburg, you have some pretty significant things that you dislike about RFK, which I think are fair. They're never going to get a chance to get aired out, because you're never going to get a chance to be put on a national platform where there will be really enough debate. And I think that's where America loses. So yeah, in that context, I would say that vvac has done more in the last month to convince me that he is fiscally responsible. And that he has some intuitions that I think RFK and Trump, and a lot of people in America share, which is just about the usefulness of the blob. And you know that there maybe needs to be a grand experiment where we deconstruct the blob. And I'm for that experiment, to be totally honest with you to see what happens.

SPEAKER_04: Sax, where you at?

SPEAKER_01: He's unhappy. What I would say, I think it's too early in the

SPEAKER_05: process to say definitively, okay, this person has to be the person for me, I'm viewing candidates as either being acceptable or unacceptable. And the vague is acceptable to me. I think distances to the ones who are unacceptable to me are the

SPEAKER_05: ones who would escalate this Ukraine war, because I think that avoiding World War Three is, to me, the central issue of the campaign. So for me, it's just a litmus test issue, I can only support a candidate who would work to end this war, not one who had escalated.

SPEAKER_04: Where does our fiscal emergency set for you in terms of priorities? So no World War Three priority one is the fiscal emergency that we're facing? Priority two? Or is it overstated by me, do you think or others?

SPEAKER_05: No, I think it's important. But the problem is this is that in order to do something about that problem, you really need bipartisan support. Yeah, because it would be suicide for one party to try and do all the heavy lifting without the support of the other. And I just don't see in the near to midterm that you're going to get that kind of bipartisan support no matter who is president, whether it's a Democrat or a Republican, the only issue that for sure, the American president has unilateral discretion over is our foreign policy. And so for me, making sure that the next president pursues a foreign policy that doesn't result in the destruction of the United States, that to me is the overwhelming issue. It doesn't mean these other issues aren't important, but look at how stunning these numbers are. Let me show you this poll for a

SPEAKER_01: second, just so we level set with the audience poll ending September 18 2023. For those of you not watching on YouTube, Trump 39% is that or 38? Then the vague 13% Haley 12% Christy 11% DeSantis 10% that is a stunning turner. Yeah, that's

SPEAKER_05: probably because it's New Hampshire, Jake out but you

SPEAKER_01: know, no, I know it's just but that's a very critical state, right? I mean, sex What do you think about what Dalio said on stage about the

SPEAKER_04: need to have a Manhattan project style effort here that is bipartisan, comes to the center and tries to resolve this as that scale of an emergency? Is that realistic to kind of frame this as we are in a fiscal emergency, we have to get a Manhattan project style effort underway to try and engineer a solution?

SPEAKER_05: Well, let's back up. First of all, I think you asked the right question to him, which is, is our decline a matter of physics, you know, due to forces we can't control? Or is it something we still have control over? And I think that that's a really good framing. I think if you're in the bucket that we can do something about it, I mean, I believe that we can. The question is how. And I think his view was that somehow you get all these elites together and you get them on the same page. I don't think that's how our system works. I think what happens is you have elections, people compete against each other, and then voters decide who's right. And so one side has to defeat the other. And I think until we get some clarity from voters on the direction they want to go, I don't think there's going to be a resolution.

SPEAKER_04: But to your point, there's no solution without bipartisan bipartisanship here. So what is the path to bipartisanship when it comes to the fiscal crisis? I'm not sure wouldn't the obvious thing be if one party wins with that as part

SPEAKER_01: of their platform, then it becomes part of the winning platform and the winning formula? Are we just saying that's not even possible because it's too unpopular to tell people that they don't get free money?

SPEAKER_05: I think it's political suicide for one party to engage in deep cuts, deep government cuts, deep cuts of programs, especially popular programs, you probably cut the unpopular ones at the margins, but it's political suicide to cut anything important without having the other party on board. There's been a couple of times where we've been able to have this type of consensus. I mean, the one that always gets mentioned is when Reagan and Tip O'Neill cut a deal. And they were able to reform entitlements and make some changes to those programs. And they kind of did it arm in arm. And that worked. And then the other time where it kind of happened, not through agreement, but almost through lack of agreement was when we had the sequester. Remember when Obama was president, and what happened is the Democrats and the Republicans worked out a deal where if they couldn't agree, you would get equal cuts in both military spending and social spending. The idea being that Republicans wanted the military spending, the Democrats wanted the social spending. And that's ultimately what happened is that they couldn't agree. And so you got the sequester and we had some spending restraint for a short period of time. The problem now is that both Republicans and Democrats want more military spending. I don't hear anybody really argued for cutting military spending, except for maybe Ro Khanna at our event, but the Democrats are completely on board with war now. And then on the social spending, I don't think either party really wants to cut social spending either or do entitlement reform. So there is no constituency out there for reigning in the biggest sectors of government spending. So I don't see how it's going to happen no matter who the president is. Well, the forcing function will be the debt

SPEAKER_04: service costs, which is just crossed a trillion dollars a year just to pay the interest and it's mounting right 30% of our debt I think is coming up for refinancing in the next 12 months and that's going to refinance at a 5% rate. That's where the markets are at. Just like consumers can ignore it

SPEAKER_01: for a burden put their fingers in their ears and say la la la la la I don't have to worry about my payments, then the payments show up and you got to worry about same thing's going to happen here in the US right the federal budget will get

SPEAKER_04: naturally constrained at some point here. But yeah, as the

SPEAKER_05: economist Herb Stein once said, if something can't go on forever, it won't. So I think I think you're right freeburg that this is a yoga bara. It's not yoga baras. I think yeah, if something can't go on forever, it won't. I think that that's where we're headed is we're going to have restraint imposed on us from the outside. It's not going to come from people. People stop buying treasuries, interest rates just have to go

SPEAKER_05: up to Japan, right? I mean, their bond auctions have been

SPEAKER_01: very lukewarm. And supposedly, a lot of the money in Japan is coming west looking for opportunities to get alpha. So we have an example that we can look to. All right, let's get we can get started here. We have so much to talk about. I think we got to give some flowers here. Last year, the Sultan of Science, the Prince of panic attacks, the queen of quinoa was an absolute terror. When I did the all in summit 2022. And then this year, he was an absolute all star in delight. What an amazing job you did on the content people are saying the content at all in summit 2023 is the best conference ever had. Bill Gurley got a four minute ovation. And that talk is on YouTube. Elon Musk star LinkedIn from 40,000 feet. He crushed it. Toby was fantastic. Ray Dalio Larry Summers Mr. B beast. Gwyneth Paltrow, the boat has sisters, which we did a pretty good show. And I have to say a great job to sacks and Friedberg, who held the line with the boat test sisters in our group chess. Brian Armstrong, who am I missing here? I mean, what an incredible lineup.

SPEAKER_04: Nicole Paul, Rob Henderson, Jenny, just Rob Henderson. I

SPEAKER_01: mean, extraordinary. Let me just go around the horn. Chumak your what what what discussion or moment pick pick your choice there. For you was the most intellectually engaging and important at the summit. You can mention two or three if you like. I thought number one were my outfits.

SPEAKER_01: Pretty great. I mean, you did do an alpha change twice a day. So Congrats on that. I like that. I did a really good job with that. I do agree. I agree.

SPEAKER_05: Did you guys get the special shoes from Laura Piana? Oh,

SPEAKER_03: the Kings cashmere loafers. Yeah, those are ridiculous. I'm wearing them as we speak. Actually, I wore them. They're kind of night. And I can wear them. Yeah, yeah.

SPEAKER_05: Shoes. clouds. They're the most like 10 pairs or something. And

SPEAKER_05: yeah, we got four special for us. Yeah. Then I get back to

SPEAKER_01: the Beverly his hotel the suite. That freeberg booked me a beautiful suite. Thank you. freeburg. And there is a Laura freeberg shafted me on my room. What? What? Yeah, I put you by

SPEAKER_03: the garage. No, I got a room that was well, it's very appropriate that these rooms exist, but it's handicap accessible, which totally fine. Except the problem is the the closet and everything is set for wheelchair height. Why did you

SPEAKER_03: change your room dude? And so all my and that's why I thought Oh, he just fucked me on purpose. He just tried to control your little passive aggressive name check. So you guys got some work to do in the group therapy. I would never do that to you guys. Don't worry. When I when I organize a summit, I'll make sure these details are perfect. I fly on to my plane. He has gluten free Nutella crepes

SPEAKER_04: handmade in the morning and I stick him in a handicap accessible room where he can't even put his bag in. And I can't

SPEAKER_03: put my clothes except without it touching the ground. So then I had to play them on the bed and then I had to lay them on the side.

SPEAKER_01: The audience right now is just triggered by the suffering that you went through at the Beverly Hills Hotel. My honest reaction

SPEAKER_03: was I thought the content was really inspiring. I guess it's kind of like, I knew what I was going to get up front with so many of the folks because I knew them. But then where I still came away where they exceeded my expectations. Number one, probably was Graham Allison. Oh, I could literally talk to him for eight hours a day, I feel like and I don't know him well. So I felt like I was scratching the surface of the things that he knew. I could do an entire dinner, I think where he could just walk through the Cuban Missile Crisis and I could just sit there listening. So I thought he was unbelievably intellectually stimulating for me. Every time I sit down with

SPEAKER_03: Toby, I'm just like in awe of how smart and different Toby Lutke is. And so I always kind of like walk away thinking this is really one of the very special entrepreneurs of our generation just in terms of his mindset. Underrated. I thought Larry had the line of the summit Larry Summers, where he said, self esteem should come from achievement, and not the opposite, which is that achievement should come from self esteem. And he was talking about wokeism and sort of like the entire philosophy around that stuff right now. And I thought that that was really insightful. Those are probably the three moments I thought girlies obviously presentation was super but again, it's kind of like saying the obvious because it was just so masterclass but the from what I expected to what I got those were the three that I thought were the most inspiring and net new positive for me. Fantastic.

SPEAKER_01: sacks. Did you have any moments aside from Gwyneth Paltrow saying she was your favorite bestie other than that being the clear number one for you and crushing soul crushing for us? Well, I never even heard that because of the zoom issues. We

SPEAKER_05: had technical issues during her interview and it got really hard to hear her at various points. And I don't think you guys heard that either. Right?

SPEAKER_01: I heard it. I tried to ignore it. I tried to block it. I couldn't I couldn't hear it. So I didn't know that. Yeah, well,

SPEAKER_05: congratulations. We can we keep that up right here? No, we're

SPEAKER_01: not doing victory laps on the pod. We talked about this on the chat. No, I mean, that's awesome. Go go for it. I don't hear

SPEAKER_00: you. My husband, but we have a little attention is to face something. So it's, it's a catch.

SPEAKER_03: Oh, my God. She's in love with David. No, that is her husband thinks that she is

SPEAKER_00: a little attention is keeping time with David. So this is not

SPEAKER_02: good. David is jealous. That's not a good situation. Reuse that. After that. What did you like sex? Be honest. I want to

SPEAKER_01: also give credit to David Sachs, who showed up for every talk. And free break said, Jake out have an issue. I said, Well, anything I can help. He said, Oh, well, actually, the issue is I asked David Sachs to show up at 845 for the run through in the he won't respond to me. Can you can you get in touch with him? I said, let me tell you what's gonna happen with David Sachs. programs just started nine, he'll be here at 856. And if you get them on stage for two out of three talks, you did better than I did. And free birds team, which God bless the production board team. They did an amazing job. These Wolverines are incredible shout out to Laura, Rachel and everybody on the team. They did a fantastic job. And sure enough, sack shows up at 856 goes on stage and he crushes it. So great job getting him on stage. But congrats on showing up for they wanted me. I mean, I asked when's the first speaker going

SPEAKER_05: on stage? Yeah, actually, it was 10am. Right? 10am. 10. So I'm like, Okay, in my head, I'm thinking, Okay, I'll be there at 959. And I'm like, what time do you? Yeah, and then they're like, you were there at 955. And I was like, there at 830 for a soundcheck. And I'm like,

SPEAKER_05: does Mick Jagger come from the soundcheck? What?

SPEAKER_01: I'm sorry, Jimmy Page.

SPEAKER_02: Here. Let's start the show. Can we have a good self aggrandizing

SPEAKER_03: ourselves? Look, I thought the conference was amazing. It exceeded my

SPEAKER_05: expectations. Your conference exceeded my expectations to JCal, but I think freebird took it to another level. Yes, he exceeded my my already high expectations. Yeah, you know, highlights. I mean, I think starting with Ray Dalio as the first speaker was really interesting. I think we only got to go for what 3040 minutes with him. I felt like we could have gone for two hours. You have to bring it back on the pod and, you know, drill into that topic more. Two hours or Dalio would

SPEAKER_01: be amazing. Because I think what's really interesting is the

SPEAKER_05: way that he's looking at the grand sweep of history, right? He's thinking about not just a 10 year business cycle or a 75 year debt cycle. He's looking at a 250 year empire cycle. I think this is really interesting that he thinks in that really big way. I agree, Graham Allison really interesting. We could have spent two hours with him. Larry Summers, these are all people I think should bring back on the pod for a long form conversation. I agree that Bill Gurley's talk was one of those great Ted style talks that I think should go viral. I think it has, you know, I think people should watch that. Yeah. I mean,

SPEAKER_01: the people retweeting it are incredible. And I was at a dinner party last night, and everybody was talking about it. So it's spread into our industry. And it's starting to tip over into other industries already. The chess was really

SPEAKER_05: fun. I am a game day player that way. You know, I brought it and managed to win the game. I don't know there are a lot of great moments. I'm sure forgetting about things. I love that. I love that.

SPEAKER_03: Parties were incredible.

SPEAKER_03: The parties were absolutely incredible. We miss both of you

SPEAKER_04: guys at the Grimes DJ set. That was amazing. By the way. I think

SPEAKER_01: Jim was there for that. weren't you there? No, I left right at

SPEAKER_03: 10 to fly back to the Bay Area early night. Yeah, I got it.

SPEAKER_01: Great. Yeah, she Grimes. Thank you to drop Grimes for doing that for me personal favor. The audience lost their minds. Santa Monica. She's such a performer. It's incredible.

SPEAKER_01: Yeah, people were losing their minds. For you freeburg. Best moments on stage.

SPEAKER_04: It was just great to be with everyone and go through it. I mean, honestly, I didn't source all these speakers you guys did. And so I don't want to take credit for that. I think it was what I had hoped. You know, I went to TED for 12 years, I started going to TED, I think 2007. And I felt pretty disappointed over the last couple of years. And I actually spoke to the CEO of TED and said, I'm not going to go anymore. Because so much of this, the talks became kind of social justice type talk nonsense that I wouldn't, I don't want to use that term. Because I do think it's all very well intentioned. And I think it just became overwhelming that you would go to TED and you would basically feel bad about yourself. And that it kind of missed the element of the world

SPEAKER_04: is an amazing place, we should have a great degree of optimism with technology and where it's taking us, we should observe the greater cycle and the bigger perspective of things that are happening in the world, not kind of go into a whodunit and who's to blame and us versus them kind of mentality, which I think so much of this stuff turned into at TED. And I was really hoping we could capture some of that. And so I'm really glad we got a lot of the speakers we did and had a couple hours to be able to share, you know, those sorts of perspectives. So it was fun. I really enjoyed what you did with the conference in terms of the

SPEAKER_01: editorial direction was great, you leveled it up, certainly from last year, as Tramath pointed out correctly, and it had a great amount of optimism, realism. And we didn't talk about superfluous virtue signaling, social justice, woke nonsense that really is should not be at the top of the agenda in my mind. I'm not saying that these issues are not important to some people. But I think prioritizing what's important in the world is what I got out of the conference. You know, when you have people on this level, speaking for for, you know, very long periods, not long enough, but you know, that Larry Summers and, you know, Ray Dalio, I mean, these talks, they really gave you a sense of this is what's important in the world right now. This is the priority. And I came away from it so intellectually stimulated, maybe just say, Hey, you know, I want to travel more, I want to read more, I want to have more conversations. And I have been basking in that, like after glow. So I just want to say, you know, once again, what an extraordinary amount of teamwork, just as the moderator of our quartet, felt everybody did a great job moving the ball around. I think everybody was on their game, everybody, you know, I'm talking about the three of you guys. Very focused on just

SPEAKER_01: knowing exactly when to insert a great question. So I felt like we were playing basketball, like the Warriors, when they play prime basketball ball move really well. Great questions, people picking up on themes, threading themes from one talk to the other. And it just made me really excited for next year. So I just want to say great job to each of you. Thank you back at you. No, I gotcha. Listen, we could talk about ourselves all day, but people hate that. Let's talk about what's going on in the markets. Yeah, we only did it for 40 minutes. Perfect. Okay,

SPEAKER_04: yeah, exactly. IPOs and M&A on fire. We've had a ridiculous

SPEAKER_01: week, six quarters of down market has suddenly turned into a bunch of green shoots on the M&A front. Cisco announced it acquired Splunk for $20 billion in an all cash deal. If the notes are correct here, it's about 10% of Cisco's market value. Somebody did a trade where they bought a bunch of options. And so that looked a little fugazi. Congratulations to Nancy Pelosi on that trade possibly.

SPEAKER_05: Don't forget your favorite word allegedly,

SPEAKER_01: allegedly, allegedly, perhaps I don't know she's good at trades. So if somebody is going to make money on that trade, or somebody's going to jail. So congrats to Screlly instacart clay vo and arm all IPO in the past week. And you know, they've fallen back to earth. Just crazy stat 21 months since the last significant venture back company went public, I'll leave out like the Middle Eastern food company was a kava that went public, and then the vacuum company that went public. But that's just in the past seven days. So we talked about this on the program. We discussed, hey, we'll know when the markets are back, if some of these companies are forced to walk the plank, slash, get public, you know, and fix their cap tables. And sure enough, instacart really kind of represents that most most of the late stage investors in instacart are underwater, the early stage folks absolutely crushed it. Chumath. Listen, you're you're a market expert here, you've taken a lot of companies public. What do you think the last week means for the greater technology industry? I don't think that this was the great reopening that we all were

SPEAKER_03: hoping for. I think it's important to understand the dynamics of bank led traditional IPOs in America. And the best way to understand them is to contrast and compare to how that same company would go public in Europe or Asia, because it'll explain what what happened. And I think unfortunately, what has happened is not good for the market. So typically, what happens is when you construct an IPO, you're selling 15 to 20% of the company. And when you do that, you go and you call hedge funds, and you call these mutual funds, but what are called long on these, right, meaning they don't short, they just go long, these big mutual fund companies. And you try to find a handful of people to anchor the IPO. So they take a huge piece of that 15 to 20%. And in Europe and Asia, the securities law says that when you get such a big allocation, you have to hold it for six months, which means you're treated exactly the same as the employees who are typically locked up in an IPO, for at least six months. And so what happens is these firms do all kinds of diligence. And when they buy something, it's because they really believe in it. And then they go long it for you know, what is at least half a year. So it's a it's a non trivial amount of time. So that's what happens in Europe and Asia 15 to 20% of the company is sold a handful of people anchor and you're locked up for six months. Now you need to look at how American IPOs are done, which is why people have experimented with direct listings. We've experimented with SPACs, it's because the fundamental architecture of IPOs are broken. They're set up in a dynamic where it's a heads I win tails you lose situation for the bankers that run the IPO. Now what happened in these three IPOs? Number one, it was less than 10% of the float. So highly, highly, highly concentrated small amount of the of the company was made available for sale. Number two, there really weren't anchors. What happened was the allocation of that less than 10% was smeared across 50 or 60 different organizations. And then number three, there was no lockup, which meant that people could sell right away. And so what you saw with all of these companies was the exact same dynamic, which was it opened, because there was such a small amount of supply, it traded up. And the minute that retail, which typically tends to be late to the game, because they don't have access to these things, right? When they started buying, what was unique this time around is all of the mutual funds just dumped everything. And the hedge funds were like, well, we don't have a real allocation. Our friends said in the group chat, he got a five or $10 million allocation in these IPOs. These are 20 and $30 billion hedge funds, five and $10 million allocations don't move the needle. So the hedge fund sold right away and got on the sidelines and said, I don't care about this. The long onlys bought just enough to make the stock go up because of such a small supply, then when retail stepped in, they just dumped it all. And so unfortunately, what's happened is all three IPOs within a few days, have breached their issue price. Now, they're at the same issue price may be slightly higher. But that is an unsuccessful dynamic. What could have been different, the banks could have forced these companies to sell up to 20%. The banks could have found a few anchor buyers, the banks could have created a lockup structure for these anchor buyers, they did none of it. And so the result is a lot of downward pressure in a moment where the overhang of rates has have come back and are forcing all of us to realize and we'll talk about it in a second that these rates are going to be higher for longer, which completely changes how you value these tech companies. So net net, very poor IPO construction by the banks, and the the grand reopening was a grand closing, I think. Okay, so

SPEAKER_01: just to put some numbers on that instacart's float was 6.7% and clavios float 7.6 arm's load almost hit the 10% 9.4 but certainly less than the 20% that you would expect. So then I guess the follow up question here, saxes, why did these companies go out? And do we see the the other big ones go out the stripes, and some of the other backed up inventory? What's what's the back channel in our industry about the viability of other IPOs? Is this going to push a lot more people out to get liquidity, even at discounted prices, even with the headwinds that Chima points out? Or is this going to have a chilling effect? And people are going to say, you know what, let me wait till 2025. So I think they went out because investors

SPEAKER_05: and others need liquidity. And there's no point holding on and waiting for a valuation that's never going to come back. I mean, so you take instacart, for example, their last private round was at 39 billion. What's the market cap now around nine, nine. So it's great that they got out. I think that is eight today today. I mean, that look, it's sort of a green shoot that they got out. But we're never going back to the valuation level. So we had a couple of years ago during a giant ZURP created asset bubble. So I just think there's no reason to wait. And you look at SoftBank, they needed the liquidity from the arm IPO. Yeah. So I think that's why these companies are going out is it's we're kind of getting back to business as usual, just to broaden out the question a little bit. What I think is interesting is that for the past year or so we've been in a software recession. It really started in the first half of 2022. The markets cratered, especially for growth stocks. There's a huge correction evaluations that happened in especially the first half of 2022. But then, about a year ago, so starting in mid 22, and continuing through Q2 of this year, you saw a reduction in growth forecasts, everybody started forecasting down. There wasn't a single board meeting that I was in, in private companies that wasn't missing their numbers and re forecasting down. And you saw it in the public companies as well. I think German ball substack showed that the average growth forecast for SAS companies for next 12 months have been cut roughly in half. So for the last

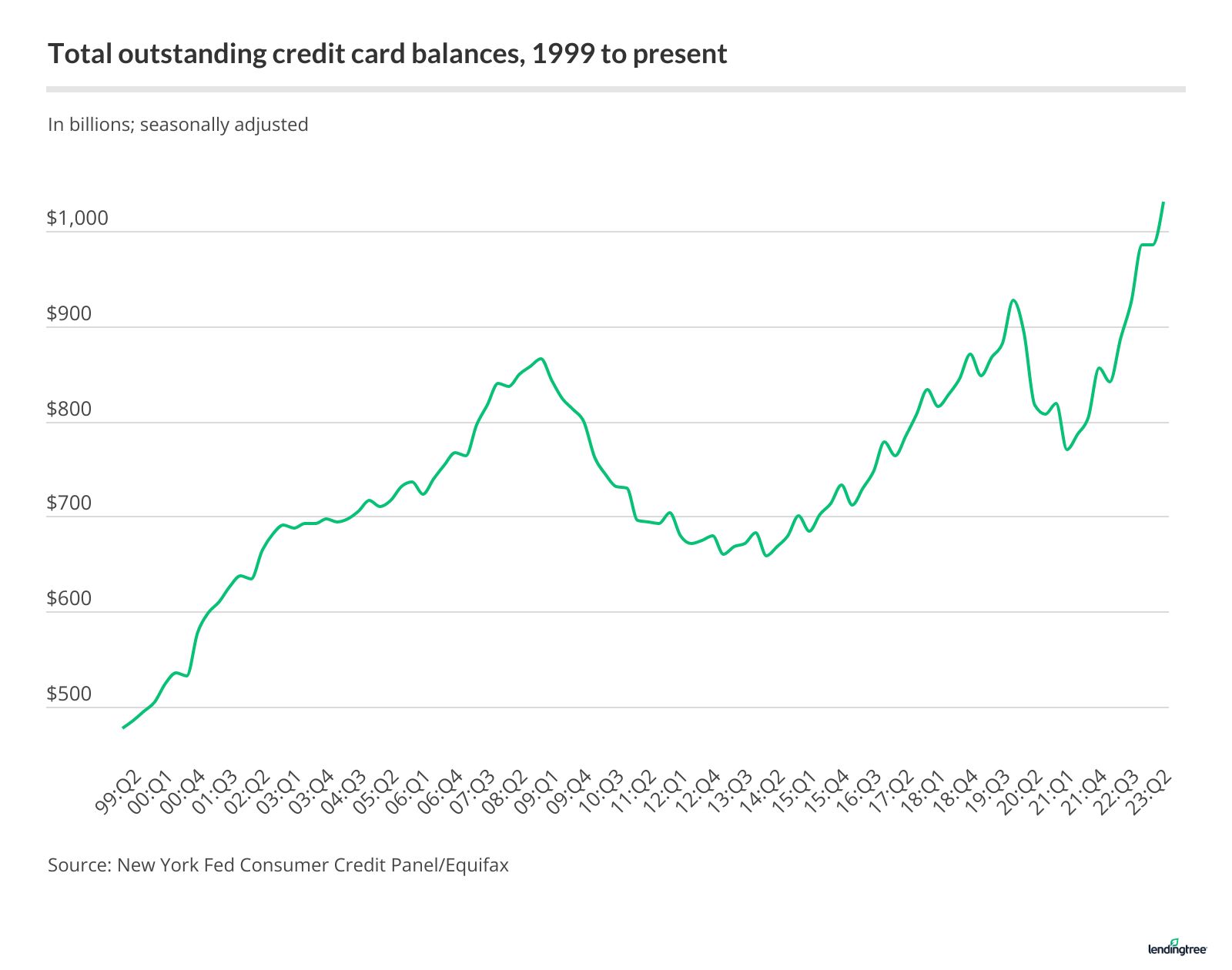

SPEAKER_05: year, year and a half, we've been in a software recession, you could say a b2b recession, we saw companies like meta, Google, and so on cut thousands of jobs, tens of thousands of jobs, you know, get much more efficient. Yeah, each that meant they were buying a lot less software on a per se basis. So I think we've been through call it a b2b or enterprise recession. But the thing that's held up stronger than I think people might have expected over the past year has been the consumer. Consumer spending has kept the economy afloat. So the b2c part of the economy has been strong, whereas b2b has been very weak. What I wonder about next is whether that's going to flip. I wonder if the consumer is on their last legs here, you see credit card debt is at an all time high interest payments on credit card debt, all time high mortgages, the rate now is approaching 8%. So no one can afford to sell their house, which has a 3% mortgage, and then buy a new one at 8%. So real estate transactions have cratered. The commercial real estate industry is, you know, on its last legs, I think they're starting to throw the keys back to the bank and start forfeiting buildings because they can't refi at an attractive rate. So I just wonder if the consumer now is about to go through the type of pain and restructuring of their personal balance sheets, the way that the enterprise segment of the economy over the past year, freeburg your thoughts on what we're seeing here in terms of

SPEAKER_01: the IPO window companies getting out and the impact that'll have maybe on how limited partners look at venture funds that's been frozen for 18 months limited partners, and I'm raising a fund right now publicly under 506 C, so I can talk about it. And it's going great. But man, it's a lot of meetings. And I'd say two thirds of the meetings I'm having, people are saying we're not adding managers, we're cutting managers, and we're cutting commitments to managers. But we'd love to meet, you know, just to start the relationship, you know. So what do you think this means overall for the limited partner, GPS, and the startup market? Start of a turnaround? Or maybe just sideways for more? I guess we should just put the volume in context. If you look

SPEAKER_04: at the slide, this is from Ernst and Young, showing the IPO activity by year, and this was through June 30. So if you assume kind of a steady state, you probably are going to come in at a volume that's less than 22. And perhaps even less than going back all the way to 2019, with less than 1200 IPOs during the year, compared to the peak of 2400, which happened in 2021. If you go to the next slide, and just look at the total dollar volume raised, so that IPO proceeds thus far through June 30 of this year is just around 60 billion. Compare that to a total of about 180 billion, all of last year, 450 billion in 2021. And the IPOs we're talking about today, Instacart, Clavio, Arm, in total raised about five and a half billion dollars. So you know, that kind of doesn't have a huge consequence on this dollar volume for the year. And then if you look at what's in the pipeline right now, in terms of what's publicly filed as S ones, there's basically nothing right now. So I think everyone's kind of sitting around waiting to see how these transactions go before they decide to put other stuff. I think the big mistake is that we continue to treat IPOs as this big yardstick. The real yardstick for a business is the performance of the business. And the valuation you get when you raise capital at some point in time is largely driven by market conditions, not necessarily by the performance of the business and the value of the business over time, the market will do its job, and rightly value that company. We've talked at length about how much value has accrued as a public company for Apple, for Microsoft, for Google 99.9% of their total market value was realized post IPO. So the IPO transaction, I think it's a little too much weight, and gets a little too much attention in terms of determining success or failure of a business and success or failure of the investors in that business. So I really hate this whole thing about does the IPO price go up on a day, it's this really weirdly engineered thing that they try and do to drive psychology and marketing by banks to go out and they the base the base to try and get people to give them more capital or to give them more deals in the future. Do you think that the IPO market would be better

SPEAKER_03: served if banks were forced to be locked? Or the the allocations were forced to be six month lock like the employees? Of course.

SPEAKER_01: Maybe longer. What if they were if they were locked for seven years? What do you think?

SPEAKER_04: Well, where would the float come from on day one?

SPEAKER_03: But why do you need a float? Yeah, I mean, that's that's a

SPEAKER_04: good point. I, I believe the direct listing should be the way that you do this. And then you do a follow on offering once you're sure it's right. The problem with the direct listing

SPEAKER_03: as I found as a seller, because I went through a handful of direct listings, I went through slack and I went through Coinbase, Coinbase, right? Yeah. And in the slack direct listing, I only sold a small portion on day one. And it turned out to be a mistake. And the reason was because the pricing of a direct listing forces you to find the absolute highest price at the open. Now, I we learned that so then going into the Coinbase IPO, what all the venture investors did was distributed literally the day before and the day of the direct listing, right, so that you would get delivered your stock at the highest price so that you could sell. I'm not sure that that serves anybody any better. You know what I mean? Because then you get a lot of price volatility, and the price just goes straight down. So I don't exactly know what the answer is. I suspect, though, that getting companies to float at least 15 to 20%, and doing a better job of allocation so that you're right, David, removing the psychology of like, it has to go up 100%. On day one is success is the thing that actually catches these companies off guard. Now, we haven't even talked for a minute about whether any of us thinks the quality of instacart and clavio and arm are good businesses. And this is part of it as well. Exactly. You just spent 15 or 20 minutes debating the stock price that is completely divorced from the reality of these businesses. And that's a bunch of distraction that the banks create as well that are that is totally unnecessary. I mean, what do you guys think about these businesses? Let me just respond

SPEAKER_04: to the direct listing point. I just want to also point out Spotify went public via direct listing the stock actually traded up after the direct listing. It went down a little bit after but it continued to trade up, you know, into the 2021 era. And today it's trading at or above what it was trading at during the direct listing. So can I tell you why though, the performance of that business fundamentally drove interest in from investors. The thing with the Spotify IPO was that it was

SPEAKER_03: still a very new vehicle. And so that direct listing was we were all learning as we went along. And at the end of the day, there was one bank that kind of not cornered the market, but really became an expert on it. And they use Spotify as the example. So by the time slack and then Coinbase came along, the playbook was so tight that everybody knew how to play the game. So I think a lot of the Spotify post IPO behavior was a bunch of people figuring out what a direct listing meant. By the time that we actually deal slack, and specifically when we deal Coinbase, the bank was so sophisticated in telling us here's what's going to happen. Here's what you should do. What do you want to do? And obviously, we wanted to do the thing that maximize returns for our LPS. So I'm not sure that the Spotify example will ever repeat in a direct listing. I think that the slack and Coinbase particularly will be the example going forward, you'll top tick day one, and then the thing will spear down, find a bottom and then why does it matter? Why does it isn't it ultimately about finding the

SPEAKER_04: real market value for the company? Yeah, it doesn't matter. It doesn't matter that the price goes down or goes up that ultimately, the buyers that want to pay a certain price will step in and buy. And the folks that want to sell because they think the price is higher than their mark will want to sell. I agree with you. I do think that it's really about

SPEAKER_03: business fundamentals. But there's a lot of people that get caught up in the price as what the quality of the business is. Now those people are maybe not the most sophisticated people in the world, but they make a lot of noise for not knowing what's going on. And so they can be a real distraction to a CEO trying to run a business. I remember in 2008, I think I've told you guys

SPEAKER_04: the story. It was like November of 2008. Expedia was trading down to seven bucks. And I saw Dara at some event in March, yeah, March, and he said, Hey, our stocks at seven bucks, I can't believe it. I mean, like, everyone should be buying our stock. And that was well off of the price that it had been trading at in 03, 04, 05. And sure enough, if you had bought that stock, you know, you would have made 15 x from there to where we sit today. And even more, if you sold at the top taken 2021. So you know, these Yeah, there's a that's a good chart. So look at where Expedia was in March of 09 is right around seven bucks. And I think that that was for me, like the first example where I really understood that the price where the market trades a stock shouldn't matter as much as the fundamental value of the business if you're willing to be a long term holder, if you're willing to say you're willing to do the work, and you're going to work. Yeah, most people are not

SPEAKER_03: willing to do the work, they want to look at a price. And then they want to imbue all of their own psychological desires into it versus what are the actual ones and zeros of a spreadsheet tell you? Yeah, but I'm like a pure efficient market

SPEAKER_04: guy, I feel like the you know, whatever shares should be, people want to sell, they should be able to sell whatever people want to buy should buy the market. And if the stock gets too cheap, there's plenty of capital out there to step in and buy the stock if they think that it's too cheap, and the market will find itself. So let's do the underwriting of Instacart

SPEAKER_01: then where any of you guys investors in Instacart know

SPEAKER_01: through any day I'm in a fund that's an Instacart from the

SPEAKER_01: seed round. So I will do I think very well because of that. Let's bleep that out. Thank you. That's that will be that'll be a yum yum for Jake out. But let's just talk about revenue.

SPEAKER_05: When it trickles down all the way to you as an LP, what's the real multiple? I guess, you know, if you take out the carry 25 or 30% less than

SPEAKER_01: what looks like to be the whole fund first. So yeah, that that

SPEAKER_05: funds been paid back many times over already. So that you know

SPEAKER_01: what the multiple is on that fund for? Yeah, it was 8 million invested. And that's their investment. That's not your

SPEAKER_05: investment. Yeah. What? If you look at your investment, what my

SPEAKER_04: understanding is that investments going to be 200,000

SPEAKER_01: 200 x 100 or 200 x somewhere somewhere in that range. I will report back but I think the seed round investors are going to be hold on. So you're saying 8 million will become 1.6 billion.

SPEAKER_01: I think it's over a billion. We can actually have a chart here. Let's take a look at let's assume it's a billion 1.6 seems a little high. Let's say a

SPEAKER_05: billion. But let's say the fund was what five 600 million. So 100 million LP, it's like a two x. I'm just saying that yeah, for the fund, it was 100 x but for the LP, it's a two x. I think that's a difference, right funds already in the black. So

SPEAKER_01: mitigating fact. Okay, so it's two extra turns of your

SPEAKER_05: investment.

SPEAKER_03: Meaning if it was a four x, Jason, he's saying that it'll become a success. Yeah. Yeah, something like that. Yeah, I

SPEAKER_05: mean, it's a good fund. I'm not disparaging it, but I just I'm just trying to set things some put things in proportion. I

SPEAKER_01: think I think at this point that funds at 21 x right now. Something in that range. So it's a pretty great fund. In terms of total to 23 x, something to that effect. Yes. It's gonna be pretty amazing. What else was in there? That was instead, Instagram, and WhatsApp were also in the fund either before it or with it. So they were pretty good fun. There were two funds. I wouldn't say which firm this is. What 12 and 24 x, I believe is the last time I checked in WhatsApp was a

SPEAKER_05: monster. That was a really well, everybody learned from WhatsApp.

SPEAKER_01: And, you know, shout out to the Sequoia team, Douglas only, I think, and they did every round. Jim gets to them. Yeah, they did every round. So it was an internal round for I think, four rounds in a row. So they just made preemptive offers. The

SPEAKER_05: reason WhatsApp was a home run is because it was so capital efficient. Yeah, it didn't burn that much. They didn't raise that much. So there's very little dilution. Yep, for everybody. I mean, and I think that's the card is how many billions do they have to raise? Let's pull up this chart here.

SPEAKER_01: This is super telling to pull up, you know, who made money. And I think this shows you what happens in a certain environment when people do not look at entry price. The series C underwater, no, no, seriously, not underwater. Everybody from F on is kind of underwater. And everybody from the series C is underwater compared to the S&P 500. Three free birds broke even and then everybody who invested in 2020 2021 actually

SPEAKER_05: lost money. General Caddis DST, D1, Tiro, fidelity, all the late

SPEAKER_01: stage folks, even Sequoia was in that late stage at series i in 2021. But it was worth 39 billion. So but that whole environment not only was it bad for all the late stage

SPEAKER_05: investors who invested a too high a price, I would argue that

SPEAKER_05: it was bad for the companies and even their early stage investors because these companies got so inefficient. The dilution is ridiculous. Yeah. The dilution was

SPEAKER_01: ridiculous. I also think you have to think about this in the

SPEAKER_03: context of what your alternative returns are. I think that we always look at these numbers. And we think we try to make judgments. But if you put yourself into the mindset of an investor, it's actually the alternative of what you could have gotten. And it's the spread between the two. That's really important. So Nick, you want to just throw up this image that I just sent you? This is an example that I saw an axios I thought that this visualization by the way, I want to try to use this visualization in the future. Because it tries to really it just paints a very wonderful let's let's sports almost this picture shows is essentially and this uses instacart as an example, but you could use it for any company, but it just basically shows you at every point in which you could have invested money in instacart. What would the

SPEAKER_03: equivalent return have been had you just invested that same amount of money in the s&p 500. And the difference between that is what you would call the alpha, right? Because the s&p 500 is the beta, meaning it is what the market's going to do, it'll be up 10%, it'll be down 4%, whatever. And so by owning the market, you get that. If you decide to not own the market and make an explicit decision, like owning instacart, then you get a different return stream. And if you compare the two, you know how much better or worse you would have been. So what this chart shows, for example, is the series F investor in 2018. If you had taken $1 and put it into instacart would have gotten 13%. But if you had put $1 into the s&p 500, you would have gotten 68%. In the series C in 2015, had you invested $1 in instacart, you would have made 153%. But the S&P would have returned 121. The difference means that the series C investor generated about 32% alpha. Now then the decision you have to make is that 32% of incremental gain over the last seven years or eight years, was it worth it, you're not liquid. And because you have to then solve for illiquidity and other things. And this is the math that I think all of the LPS will be engaged in, they'll be doing these calculations. It just goes back to what Saxe's point said, which is, our business, frankly, did very well in moments where we had zero interest rates. Our business now when prevailing rates are at five or 6%, and you can own those things, or you can own structured credit for 11 to 13%. Our business unfortunately does not look so good. And when people do the calculations on what the true alpha of venture capital is, they're going to come back with answers like this, which is it's not that great. And I do think it will impact how limited partners have an appetite to give all of us or you guys folks that are that are accepting LP checks, more money, because the alternative universe is more liquid. It's less volatile. And it has roughly the same amount of return, I can

SPEAKER_01: tell you what they're saying, because I'm doing about a dozen LP meetings a week. And I've got 50 more on the calendar to the end of the year. So I'm going to hit 100 of these meetings, they're really saying two things. One, we want to go earlier, we don't want to go later, as that chart proves. They're suddenly fascinated with the seed and series A rounds. And they're looking for distinctly different strategies. They're looking for some sort of edge. So the first two questions are how early are you getting in and securing a 10% position in this company? And then what's your edge and literally the start of my pitch deck now, when I walk people through it is I have two podcasts, one of them gets 50 million listens a year, the other one gets over 50 million listens a year, those hundred million listens result in 20,000 applications, I have larger deal flow than anybody, with the only exception being Y Combinator. And that resonates with folks. But if you're somebody who's got a new fund, and you're like, what's your what's your edge? Yeah, I go to, you know, some demo days, that's not an edge, you have to have a massive competitive edge and a differentiate, you have to be differentiated in some very credible, believable way. And they're telling me the same thing. They're cutting two funds out of their 20. And then they're cutting their commitments to the weaker ones of the other 18. I have a question for all of you guys.

SPEAKER_03: You had a wonderful question, which we never touched guys. What do you guys think about the arm business model or the clavio business model? Let's go to Instacart. Have you guys had a chance to look at any of those companies and think about that?

SPEAKER_01: Let me tip the facts and then you guys respond. The revenue is up 15% year over year 716 million ad revenues 206 million that's on pace to make up 28% of their revenue. This is just the last quarter I'm talking about it right here and to June 30. Net income 114 million, they have 600,000 Instacart shoppers, those are like the drivers, you can think of them like doordashes or Uber drivers 7.7 million monthly active orders. The red flags is that their gross transaction volume, which is the value of all of the groceries in the in the bags is flat, but ad revenue is growing. This means ad revenue is just a massively larger percentage of the total revenue. They think they can you know, they're on track for 800 million in ad revenue. So this is starting to look not like a e commerce business, but more like a an advertising business. Your thoughts, free burger sucks on the actual car business.

SPEAKER_05: Amazon, by the way, has a dynamic to now have you seen the charts showing advertising on Amazon compared to the entire internet? Yes, it's huge. And also, Uber's blown past a

SPEAKER_01: billion, I believe here's what we know, we know that advertising

SPEAKER_03: multiples, broadly speaking, have contracted, right. So I think that the market in general, doesn't love that revenue quality, because it's too levered to interest rates in the economy. So when the economy does well, more companies advertise when the economy doesn't do well, companies advertise less. That's number one. And number two, the ones that can systematically drive advertising more broadly, the Facebooks and the Googles of the world tend to get an increasing share. So advertising as a revenue stream, I think is, is good and complimentary. Unfortunately, the markets don't necessarily love it. And then the second thing, generally speaking, for these businesses that drive huge GTVs, gross transaction values is, I think most people when they try to find what they're worth, are very sensitive to the take rate. And what they typically do is they assume a falling take rate, which means what percentage of the transaction can you get. And the reason why most people do that is that history has shown that these kinds of businesses cannot defend take rate for a very long period of time. Whether it's for competitive pressure, or whether it's because their suppliers actually develop more pricing power, take rate tends to decay. So said in, you know, in grocery land, I think it's because Walmart and Amazon will try to do it for much, much cheaper and or charge, just be more aggressive in how much they they want to keep, which means it's less that you can maybe necessarily pass through. I don't know the Instacart business at all. But if I were starting to look at it, that's where I would focus is, what are the assumptions on take rate. And if the take rate is going up, and it would be a little bit of a head scratcher, I think that you have to model the health of the business with a decline. I can actually share,

SPEAKER_01: yeah, I can actually build on that pretty easily, having spent a long time in the advertising market, if this was very profitable advertising, Shemagh, it would get a 25 x multiple on earnings. Let's take that 800 million, you put it at 400 million in profits, like if the other business didn't exist, so you have 400 million in profits of advertising times that by 20, you get a billion. That's exactly their market cap. So it perhaps what you're saying is exactly what the market is, is actually penciling out Google, which obviously has a lot of other technologies, I think a 28 x PE. And Facebook is crushed it like 35 p, but these are much different scale and scale matters. This is not one or 2 billion in you know, a little extra revenue on top of your business. That's the entirety 90 95% of that I think what's working in favor of instacart

SPEAKER_03: is that if you compare it to probably Uber and DoorDash, or Airbnb, at least Airbnb dash, I'm going to guess that it looks pretty cheap. Now, I think of all the three businesses dash probably has the biggest upside, quite just like, again, parms length, I don't I don't know any of these three stocks, I'm just saying business model quality dash seems infinitely scalable. Airbnb, I think probably has long term issues with take because of this exact reason, because just competitive dynamics and pressure regulatory capture, you're seeing that in New York for Airbnb. And then the question is, what is the business outside the United States look like for instacart? I don't know. But if I had to figure out what to pay for, that's how I would kind of try to break the problem down. Sax, any of your thoughts on the actual business here? Or do you

SPEAKER_01: want to jump over to clavia?

SPEAKER_05: Yeah, I think clavios here, the really interesting one, at least from my standpoint, because it's a software business. I think Jason Lemkin had the take here. He said that clavios IPO will be the ultimate yardstick for SAS and 23 and 24. top growth, top margins, top founders going to cruise past a billion in ARR, whatever multiple they end up trading at your home is certainly worth less. I think it's trading at about 12 times for revenue. So just here last quarter, they did 165 billion as our 65 million,

SPEAKER_01: sir.

SPEAKER_05: Yeah, so they're at 650 million in ARR growing 56%. That's amazing. So you're over year 51% of the year. So you know,

SPEAKER_05: project that for they're probably going to be at a billion in ARR next year. 119% nrr, which is very good, especially considering that folks, it's not revenue retention. It's the way to think about that is if you just look at your existing customers, going into next year, what percent of that subscription base is going to be there. And if it was 80%, it would be 20% of your customers are turning away. If it's 119%, it means you have expansion from your customer base. In other words, your customers are buying more. And there will be some who churn, but the ones who are expanding more than make up for that, and then they've been very capital efficient. Apparently, they've only burned 15 million today. That does not mean they've only raised 15 million, they've raised several hundred million in various growth rounds, but they still got that money in the bank. So I assume they raised it as a cushion in case they missed their forecast or something like that.

SPEAKER_01: Yeah, it seems like a pretty strong business.

SPEAKER_05: But I think his point is right is that they're kind of the ceiling, you know. So I think founders still have maybe unrealistic expectations from the days when SaaS businesses were being valued 100 times ARR. Have you had this conversation, Sax, with folks coming in for

SPEAKER_01: funding who have great businesses, or let's call them good to great businesses somewhere in that zone, there's seven, eight, nine businesses, but their valuations are way off. And do you do you bring up, hey, here's what your your company would be worth publicly? This is what your last round is and then trying to negotiate in between those two numbers because it does seem like founders are bringing that up proactively in some meetings with me. They're actually aware of public comps now and they're kind of admitting. Hey, I get

SPEAKER_01: it kind of situation. Yeah, I think founder expectations have adjusted on

SPEAKER_05: this. Yeah. Which is healthy. Yeah. When you're in a hot market, there's definitely a lot of sharing among founders of what's happening and where valuations are at. And I think the same thing is probably happening in the down market as well. So yeah, I think everyone's getting more realistic. Yeah,

SPEAKER_03: just to finish on clabby. I just want to give a shout out to Toby Lukey. The best thing that I saw about that was that Shopify actually owns like 11% of this company, which I think like if you look at the corporations, again, just doing an incredible job of building an ecosystem, not only does Toby support these companies, but Shopify ends up owning a huge non trivial portion. I think Shopify owns like 11 or 12% of Clavio. I think with the sale of the flex port, deliver back to flex port, they own 13 or 14% of it. I suspect they probably own a non trivial share of stripe. I say it's incredible. Right. And actually, if you do some of the parts on Shopify, their cash in cash and cash equivalents are only valued at like two or three billion. So I feel like there's a ton of upside there just for free. Again, I don't own it. I haven't done the work, but I'm just saying seems like seems like

SPEAKER_05: so I think that brings up a really interesting point, which is the only vulnerability or negative I think about Clavio's business is the fact that 70% of it is on Shopify. So that's a platform dependency. And whenever 70% of your business is on one platform, you always have to be afraid of getting the rug pulled out from under you. By the way, that was PayPal's problem back in the day. 20 years ago, 70% of our business was on eBay. eBay had a competitor, we're constantly worried that they were going to pull the rug out from under us. If we could have made a business deal with eBay, we would never have had to sell the company, it would have been ideal. I think Clavio was really smart, creating alignment with Shopify, by letting them invest, giving them equity, doing a rev share agreement. And they would be smart to continue that rev share agreement into the future to take this risk off the table. Because investors do not like existential risk, you could have a perfect business. But if there's some hard to quantify risk of the whole thing, basically getting rug pulled, then how do you discount that?

SPEAKER_03: David, as an investor, you look at that, and you're like, Okay, I then price this company as a function of Shopify.

SPEAKER_05: That's a good point. I mean, 70% of the business is Shopify. The way I would look at it is, I would price it as a SaaS business, because Shopify is more of a transact. Well, they're a transactional slash SaaS business. Clavio is a pure SaaS business, I'd price as a SaaS business. But I would have to create some sort of discount for the chance that well, Shopify adds the features.

SPEAKER_01: How do you figure that out? That's a really complicated

SPEAKER_05: thing to figure out. Yeah, I agree.

SPEAKER_05: But I think that Clavio mitigates the risk to the extent they do this like rev share agreement. It's a really savvy move for people who have insights into

SPEAKER_01: the market to own pieces of emerging companies and lock in that partnership. This was Emil Michael, a shout out at Uber and Travis did this with all of the grabs, DDS, etc. And then Dara just slowly sold those positions. And they were incredible cash accretive to that stock and to running that business. Let's talk about air table for a second. This also trended on Twitter with the tweet storm. If you don't know what air table is, it's kind of like, what is it? It's like Excel meets a database and it's more programmable. So if you wanted to have a bunch of data, a lot of small businesses use it, medium sized businesses and they use it to let's say, instead of hiring somebody to build a database system, or Google Sheets on steroids, it's actually a really good product.

SPEAKER_04: And it's a really sick product. I've seen it used like 10

SPEAKER_04: different ways. Some people use it for tracking product feature requests. And you know, task lists, some people use it for contact database, some people use it for complex project management, it's super extensible, super easy to use great collaborative tool. Like, it's like a spreadsheet for words instead of numbers.

SPEAKER_01: Yeah, yeah. But you could also do numbers. So yeah, with a lot

SPEAKER_04: of great features that you can do really dynamic things within the spreadsheet. Do you guys believe in this Swiss Army knife

SPEAKER_03: approach of building these kinds of things? Or do you believe that it's just cheaper and simpler to build best in class versions of each of those use cases freeburg that you just think it allows certain businesses to have a very

SPEAKER_04: specific tunable version of what they need from call it a project management tool. So if you use a traditional project management tool, it may be too overbuilt, or it may be too specific, whereas this tool allows you to build something unique for your platform. So that's where I've seen a lot of teams use it instead of other tools like JIRA, or whatever for track. Well, I just wonder that you get these small non

SPEAKER_03: scalable use cases, because then if a company is successful, don't they then just migrate to JIRA, for example, no, I would a

SPEAKER_04: lot like spreadsheets. Basically, the reason people use spreadsheets for so many different things is because everyone's got their own representation of data and utilization of a spreadsheet. And I think this is just an extension of that. It's a cult think about it as a more feature rich spreadsheet tool. I actually think that Jamal's question is an excellent one. I

SPEAKER_05: tweeted many years ago that the way I saw Excel was the long tail of use cases that hadn't moved into a dedicated SAS app yet. That's interesting. Yeah. And that the way that if you

SPEAKER_05: want it to be a SAS foundry, you're trying to come up with ideas, find some really complicated Excel spreadsheet that's used to different businesses. Yeah. And just figure out if you can move that into a SAS app. So for example, think about harder, you know, before card appeal, just use a spreadsheet for the capital and every company totally had a cap table. Totally, totally. But they just move that into a specific SAS app. So I think there's a lot of that. And so

SPEAKER_04: at all a spreadsheet is it's a visual representation of a database with some relational logic that you build into the cells of the spreadsheet. And this this pattern of breaking

SPEAKER_01: apart, breaking apart a major product was the playbook for Craigslist. People looked at Craigslist and said, Oh, there's couch surfing make that Airbnb Oh, there's a ride sharing. I'm going to LA I have two extra seats. That became like Uber. So people this playbook has a visual of that too, where every

SPEAKER_05: category on Craigslist became its own. Yeah. Oh, it was one. Well, you know, everybody uses free break.

SPEAKER_01: Everybody uses something different. That's interesting that it comes to that's the one that comes first. Craigslist was

SPEAKER_04: a huge dating product before dating apps came. It was casual encounters or missed. What was it called? Missed

SPEAKER_01: connections, missed connections, missed connections, missed connections was hilarious to read. It was like me you the number four trend. The point I think the point though, the question that I was

SPEAKER_03: asking is exactly this, which is you have these beefed up workflow things that happen in Excel. But then eventually you go to the systems of record that are purpose built to solve the use case. And if the use case is important enough, it just seems like that's what's happened. I don't have a view because I've never used the product. But I wonder whether part of this valuation reset doesn't reflect that dynamic.

SPEAKER_01: It is a dynamic. The two companies or two or three companies that represent it best is there's a product called coda, which is part wiki, part air table, part database, and it's programmable and notion. And now people are making templates in notion. And then they're adding things like project management. So I asked my team to do project management for events. And they tried base camp, they were looking at Asana. And then somebody was like, you know what, I just added it to notion is good enough. It's not as good as those other two products, but it's good enough. And we don't have to and the reason they want to do is not because we're cheap. I don't want to spend money on another sass product. We don't want to have to teach everybody a new sass product. We don't have to want to do the logins for that. So I think it is a natural tension and people are doing both. Juma fill. Some people like the best of breed. But we're also seeing it I don't know if you saw this past week slack added I think during dreamforce the ability to give you an AI summary of everything you missed and then zoom added AI summaries of calls. So that feature that I guess otter and some other people were doing that feature is now built into zoom, you get a transcript from zoom for free, and now you get a summary of the call for free. That is work that was done by somebody on the meeting, right? Somebody was responsible for being the note taker. Sometimes somebody was. So those are jobs that are gone. And I think it speaks to the bigger economy. I had the CEO of kayak on this weekend startups this week, it will come out next week. He's really great. And I asked him about hiring and the size of the company said I'm not hiring anybody in the next year or two. Because all my developers are 30 or 40% better. I got junior developers that are acting like senior developers. I got senior developers who are turning into 10 x developers. We're not hiring. We're just going to have increased margin. So what happened to air table? air table had a massive valuation. Here's the tweet storm. That somebody from CB insights this guy and on who I think I follow him. Did something happen or nothing? Well, they're most recently valued at 11.7 billion in December their 2021 series app. His thesis not only is air table worth less than 11.7 billion, it's likely worth less than the 1.4 billion in funding it has raised to free birds from bringing this point up over and over about the overfunding and cash in is less than the valuation most Yeah, most of these unicorns are worth less

SPEAKER_04: than their total press stack. This is a good example. I've just been through this this week I went I saw it as a company I was an investor in that I saw this happen. Para table on track to do their big problem is that I mean,

SPEAKER_05: they're doing over 100 million of ARR. It's a it's a great product and 150 million of ARR. That's no small feat. The problem is the growth rate, I think it's only 15%. What do you

SPEAKER_04: do with the founders sex because this was my point earlier, is in these circumstances, it's still a good business, investors are going to want to own these shares at some price, someone will buy new shares at some price. But to do this transaction, given that the preference in the company, which is effectively debt is greater than the value of the company, the founders and the employees get their ownership stakes wiped out. So if you want to think they're only

SPEAKER_05: I think their only hope is to go public because that wipes out the prep stack and everyone basically disowns their percentage of the company. If they don't go public. And if the found private investor do that, why would a preferred investor

SPEAKER_04: allow that to happen? Well, this is going to be the huge tension

SPEAKER_05: on the board is that if you're a common holder, or if you're one of the early investors of the company, you want to go public. If you're a late stage investor, you don't want to give up your preference. But those late stage people sacks did not have

SPEAKER_01: blocker rights in many cases, because the market market was so hot, they just put the money in without. Yeah, I mean, unless

SPEAKER_05: they had a ratchet into the IPO, but yeah, yeah, but in many cases, but that's not a universal truth,

SPEAKER_04: right? It's in almost in the majority of these cases, the preferred shareholders do have significant representation on the board, they do have the ability to influence whether or not the company is going to go public. And there's likely some middle ground that every company ends up having to meet at, which is we're going to recap the company in a way that we're going to give some shares, newly issued shares to founders, what we saw, or dash door dash disaster. Yeah, that indoor dash, I think they all

SPEAKER_01: just got dragged out. They didn't have a choice. My understanding of some of these late rounds during peak zerp 2020 21, from talking to Bill Gurley, was people did not negotiate those rights, those rights, the blocker rights weren't available. And if the majority of common says we're going public, you're going public. And that's the that's the end of the story. Here's here's the punch line to the air table. If you look at the Ford price to sales multiple 78 x for an $11.7 billion valuation at 150 million ARR, and you compare it to the trailing price to sales multiples in the

SPEAKER_01: project management space Mondays at 12 x plus a sauna 6.6 x and smart sheets at just around eight x. So it's a challenge.

SPEAKER_05: Yeah, well, to freeberg's point, one of the downsides of taking all this excessive capital at these ridiculous valuations is that it produces a dynamic in your boardroom, where your board members are at war with each other, the late stage investors are gonna be at war with the early stage investors and the founders. And who knows who comes out on top of that?

SPEAKER_04: I don't know if you guys have but I've got like so many anecdotes over the last couple of months on this exact scenario playing out. Well, take us through an amalgamation of

SPEAKER_01: those, you know, without talking about specific ones, but you know, you can make your imagination, what is the dynamic? And how does it work itself out, investor invested a multi billion dollar valuation, the

SPEAKER_04: company is now worth 20% of that valuation. And the investors have more money in the company than it is worth. And the company needs more cash. They can't go public at this rate, because the markets are shut down, no one's going to buy new shares, they can't raise cash by going public. So they have to raise cash in the private markets. So then the tough question is, okay, what's the value of the company in almost all of these cases, the CEO has been replaced, or they're with some professional CEO. So there's a new option pool created equal to 10 to 15% of the company, new options are issued, and around is done at a significant discount. And there's a huge recap and a pay to play. And all this other sort of stuff starts to play out that the original founders in the company get wiped out most of the management team leaves, because their options are now worthless. And the investors who historically have been totally passive late stage investors have had to step in and try and take action and rebuilding a management team, which guess what they're not necessarily good at. And so it ends up becoming this really nasty unwinding of the business, because everyone thinks, Oh, well, I deserve to get a fair deal, because I put money in and I have a preference in this company. founders don't want to see their ownership go down from 20% to 2%. They're like, why would I keep working for 2%? I'm fully vested. I'm going to leave the management teams like, wait a second, I'm getting offers left and right to go join other companies. And so it's a real kind of nasty unwinding. And I think that's the scary scenario that's likely going to play out not all but a good chunk of these companies that are there are still businesses, they have decent value to their business, but they just raised too much capital relative to the valuation of the business today. If you looked at it on a blank piece of paper, these businesses

SPEAKER_03: look incredible at whatever the true valuation is today. But if you have the psychological hindsight bias of what the price was two years ago, you just can't see that. Can't get it totally can't get by the way, I will say the structure there's like legacy structure in the cap table from

SPEAKER_05: yeah, meaning there's like this prep stack.

SPEAKER_04: I will say that the terms are so crazy good for the recap that investors are clawing their way into the recap. Well, that means that nature markets are healing. That's means we're in the end

SPEAKER_01: game, right? That's part of what's happening. Part of what's happening is it's

SPEAKER_05: totally predatory. It's totally predatory. When you're going to be able to go public again, I think that when there's a recap, and the founder is still running the company, there's a chance of it being fair. But when they bring in a new CEO, who then does a recap, oh, yeah, they don't care. They don't care. They don't care. Exactly. And all these recaps turn into a disaster. Yeah, well, it's recap, or you're going to go out of

SPEAKER_01: business. So I mean, this is a force and function and everybody party too hard. I think it's time for everybody's favorite part of the show, which is to give chamath his flowers. Here we go. chamath the Fed spoke this week. And it's time for chamath to take his victory lap. Here he goes. Everybody. chamath is this Holly houses. This is Vangelis. Yes, Vangelis doing chariots of fire this week. The Fed said to quote chamath. Well,

SPEAKER_03: this guy Peter, this is this is but interest rates would connections to the deep state for longer. There he is there chamath leading the pack. I sent my I sent my talking points from six months ago to my deeps up to our friend deep state can deep state sent the note and deep state sent it to the Fed and

SPEAKER_03: the Fed just cut and pasted it into the race will stay higher

SPEAKER_01: for longer. We're gonna get right on this. We don't care.

SPEAKER_02: Yeah. Who cares? I don't think anyone understands what it is

SPEAKER_05: that chamath said they say taking the victory lap on once you said that rates will stay higher for long girl. And now he

SPEAKER_01: takes his victory lap. Alright, enough of this shenanigans. chamath said rates will stay higher for longer. The Fed said rates will stay higher for longer. The end. Congratulations, you got it right. Thanks. Okay. Well, let's talk about give our chariots of fire.

SPEAKER_02: Here is a medal in the group chat.